Deciding to stop using a credit card can be a big financial choice, influenced by different reasons like wanting to reduce debt or avoid fees. If you have a Credit One card and are thinking about canceling it, it’s important to be careful so it doesn’t hurt your credit score.

Canceling a credit card isn’t just cutting it in half; it needs a careful approach to keep your financial health in check. This guide will take you through each step of canceling your Credit One card, from thinking about it to closing the account, so you know what to do at every stage.

How To Cancel A Credit One Card?

The simplest way to cancel a Credit One card is by calling customer service. You can also cancel by sending a letter and mail. Unfortunately, you cannot cancel online. To summarize, you can cancel your Credit One credit card by:

Cancel By Phone

Call Credit One customer service at (877) 825-3242. Make sure you’re in a quiet place and have your card information ready.

When you get connected, you’ll probably hear a menu with options. Pay attention to the choices. If you can’t find a way to cancel your card directly, don’t worry.

Instead of waiting a long time or getting confused by many choices, keep pressing “0”. This will usually help you skip automated systems and talk to a real person directly.

Credit card companies like Credit One usually have ways to try and keep their customers from canceling. When you talk to a representative and say you want to cancel, they will probably offer you things to try and convince you to stay.

These could be things like lower fees, less interest, or other benefits. If you have already decided to cancel, stick to your decision. Politely say no to their offers and tell them again that you want to cancel.

Cancel By Mail

Start by writing a simple and straightforward letter expressing your desire to cancel the card. Use a professional tone and make sure your request is clear and easy to understand.

In your letter, be sure to give the necessary details to identify your account. This should include:

Your complete name is shown on the card.

Please only provide the last 4 digits of your card number. Do not include the entire card number for security purposes when writing.

The address you currently have is linked to your account.

When you finish writing your letter, put the recipient’s address on it.

Credit One Bank

General Correspondence

P.O. Box 98873

Las Vegas, NV 89193-8873

Safety Precautions: Because the content is sensitive, it’s a good idea to send your letter using certified mail or another method that lets you track it. This way, you’ll have evidence of your request and can make sure the mail gets to where it needs to go.

Remember, canceling by mail takes longer than canceling by phone. This is because it takes time for the mail to reach Credit One, for them to process it, and then for them to respond.

Make sure to keep a copy of your letter for yourself. If you don’t hear back from them within a few weeks, you might want to call and check on the status.

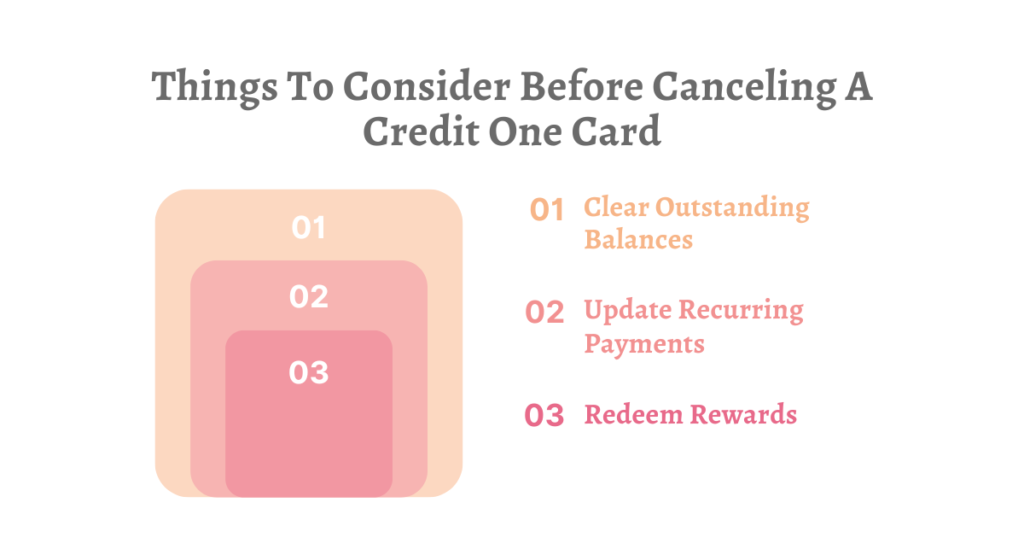

Things To Consider Before Canceling A Credit One Card

You need to know that if you don’t activate your card within 14 days after you get it, Credit One will close your new account automatically.

Also, once you’re approved for a card, Credit One will tell the major credit bureaus about your new account, whether you activate the card or not. So, if you cancel a Credit One card before activating it, the closed account will still show up on your credit report.

If you cancel your Credit One card before activating it, you won’t have to pay an annual fee. Even if you activate the card, you can still cancel it and get a full refund as long as you haven’t made any purchases.

After you cancel, there are some important steps you need to take.

1. Clear Outstanding Balances

Ongoing Responsibility: Even if you cancel, you still have to pay any remaining balance on your Credit One card. It’s important to keep making at least the smallest required payments each month.

Interest Accumulation: Remember that if you don’t pay off your balance, you will continue to accumulate interest. So, it’s better to pay off your balance quickly to save money in the future.

Final Closure: Your account will be officially closed only when you have paid off the entire balance.

2. Update Recurring Payments

Identify Automatic Charges: Check your credit card statements to find any regular payments or subscriptions, like Netflix, electricity bills, or gym fees.

Change Payment Methods: Switch payment methods in advance to prevent service interruptions or additional charges for late payments.

Notify Service Providers: Contact each service provider to inform them about the changes you need to make in your billing information.

3. Redeem Rewards

Check Reward Balance: Before you cancel your card, make sure to check how many rewards you have.

Ways to Use Your Rewards: Find out how you can use your rewards by getting cash back, buying merchandise, or getting credits for travel.

Expiration of Rewards: Keep in mind that if your account is closed, you will lose any rewards that you haven’t used.

What Happens After Cancel Credit One Card?

Even if the cancellation of the credit one card is approved, if you still owe money, you need to keep making the minimum monthly payments until you catch up. Your Credit One account will not be closed until you have paid off the entire debt. So, how can I close my Credit One account?

But, even though the account is still active, you cannot use the credit card to make purchases. If you try, the transaction will be rejected. Also, make sure to update the payment method on invoices that still charge the Credit One card.

If you still have any unused rewards, make sure to use them before you cancel. Once you cancel, you won’t be able to get or use them anymore.

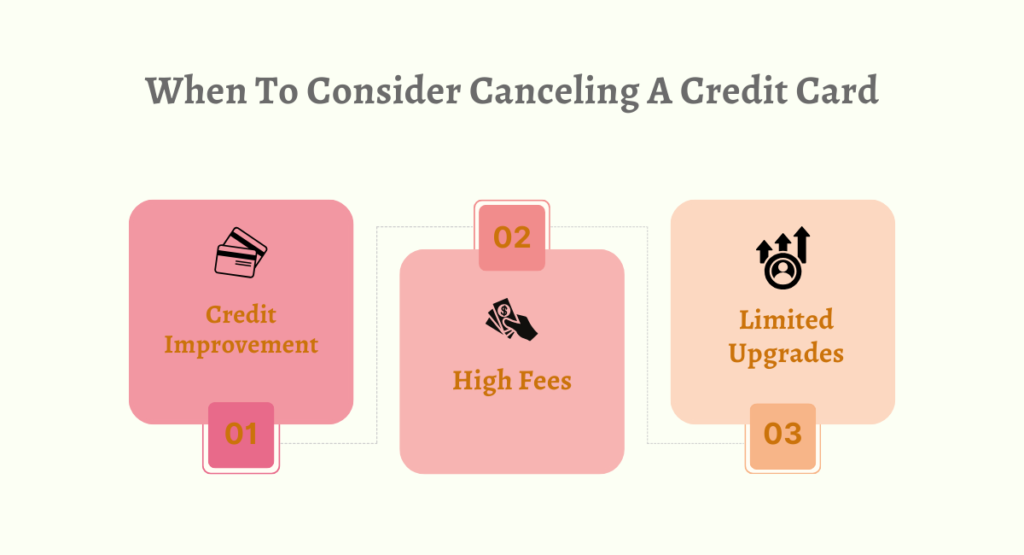

When To Consider Canceling A Credit Card

Credit Improvement

If your credit score has gotten much better since you got your Credit One card, you might now be able to get credit cards that have better terms, like lower interest rates, nicer rewards, and no yearly fees.

Improving your credit card can be seen as a positive step in your financial journey, showing that your creditworthiness has gotten better.

High Fees

Decide if the fees for your Credit One card, such as yearly fees, are worth the advantages you get. If you’re paying more in fees than what you’re getting in rewards or benefits, it might be a good idea to find a cheaper alternative.

Look into different credit cards that provide similar advantages without the expensive charges.

Limited Upgrades

Credit One may not have many choices for upgrading your card, especially if you no longer need a card to build your credit.

As your credit gets better, it’s a good idea to look for credit cards that give you more rewards, let you spend more money, and offer extra benefits.

Closing a Credit One card, just like any other credit card, needs to be done thoughtfully and methodically to avoid any negative effects on your credit score. By following these steps, you can make sure the process is done well and protects your financial future.

Thanks for reading. I hope you find it interesting.