Certain credit cards assess a surcharge called a “foreign transaction fee.” This is determined by a predetermined percentage of the foreign currency purchases you generate, including those made during your travels. Foreign transaction fees may also apply when purchasing online from an international vendor.

In this analysis, we shall focus on the Chase Freedom credit cards in particular and deliberate on the foreign transaction charge that may be incurred when utilizing one of these cards abroad.

What Is A Foreign Transaction Fee?

Foreign transaction fees are charges incurred when purchasing items denominated in a foreign currency or through a foreign bank; this includes online purchases from non-U.S. websites. In addition to debit and credit cards, foreign transaction fees can occur when using an ATM outside the United States.

Do Foreign Transaction Fees Matter?

While 3% of each transaction may not seem like much, it can quickly accumulate during an international trip or when several substantial purchases are made in foreign currencies. If your vacation budget is limited to $1,000, you want to spend something other than an additional $30 on extra fees. Fortunately, rewards credit cards without foreign transaction fees are readily available.

Several additional Chase credit cards exempt foreign transaction fees. This issuer carries an extensive selection of travel credit cards.

Several no-annual-fee credit cards outside the Chase family provide 0% foreign transaction fees.

In the end, foreign transaction fees may increase the cost of travelling or online purchases with a particular credit card. When you travel or make purchases from online retailers that operate in a currency other than U.S. dollars, it is prudent to be mindful of these fees and select an alternative credit card that does not impose them.

Does Chase Freedom Flex Have Foreign Transaction Fees?

The foreign transaction fee for Chase Freedom Unlimited is 3% of each transaction in U.S. dollars. Similarly, its companion card, the Chase Freedom Flex, does. This results in a 3% fee being deducted from the overall quantity of the transaction. Including transaction fees is not limited to the purchase price that incurs the fee. Therefore, a $100 purchase subject to a 3% foreign transaction fee would incur a $3 fee for $103.

Foreign transaction fees apply to all exchange rates using currencies other than U.S. dollars. Additionally, this fee may be assessed if a foreign bank processes your transaction.

How Do Foreign Transaction Fees Work?

An overseas transaction fee may be assessed if you purchase a domestic credit card while physically outside the United States. Nonetheless, international transactions from within the United States are also possible. For instance, the credit card company may classify an online purchase executed in a foreign currency as a foreign transaction.

A bank card with a foreign transaction fee can be identified by consulting the cardholder agreement’s pricing and terms document. Generally, the terms and conditions are enclosed in the envelope that accompanies the tangible card.

A link to the credit card’s terms and pricing can also be found on its website. Fees for international transactions are typically detailed in the “Fees” section, labelled “Transaction Fees.”

In most cases, the absence of a foreign transaction fee listing in the pricing and terms documentation indicates that the card does not impose such a fee.

How Do You Avoid Foreign Transaction Fees?

There are numerous methods to circumvent these charges, such as:

1. Apply for a bank credit card with no foreign transaction fees.

As a card member benefit, certain credit cards (such as most travel cards) do not impose foreign transaction fees.

2. Exchange cash before leaving the United States

While abroad, you can avoid transaction fees by making all purchases in cash. Before departure, you can exchange U.S. dollars for the most significant currencies at banks and exchange shops.

However, this option has a degree of risk, as the cash could be misplaced or stolen. As a precaution, using a different payment method, such as a credit or debit card, is advisable.

3. Create a bank account with no foreign transaction fees.

While travelling internationally, you may encounter a merchant who charges an additional fee for credit card transactions or does not accept credit cards. Consequently, obtaining a debit card from a financial institution that waives foreign transaction fees might be prudent. Consider opening a checking account that permits international fee-free debit card usage before departing the United States.

If you prefer to keep a current account, inquire with your bank about the availability of ATMs in the countries where you intend to travel. Withdrawals might be possible at that location without paying a fee.

4. Shop online with international merchants that accept U.S. currency.

One can circumvent foreign transaction fees by exclusively transacting online with international merchants compatible with U.S. credit cards and providing payment in U.S. currencies. Before making a purchase, make sure that the online retailer is headquartered in the United States or accepts various payment methods, including U.S. dollars.

3 Tips For Using Your Card When Travelling

Consider implementing the following three suggestions when using a debit or credit card abroad:

- Let your issuer know you’re going on a trip: If your issuer recommends enabling travel notifications, inform them of your absence before departure so they do not suspect that your activity while abroad is fraudulent.

- Know your fees: Verify the card’s terms to determine whether foreign transaction fees will be assessed. You will avoid unexpected costs upon coming home with your statement.

- Avoid dynamic currency conversions: Attempt to prevent dynamic currency conversions, as doing so will almost certainly incur higher fees than if you delegate the conversion to your card issuer.

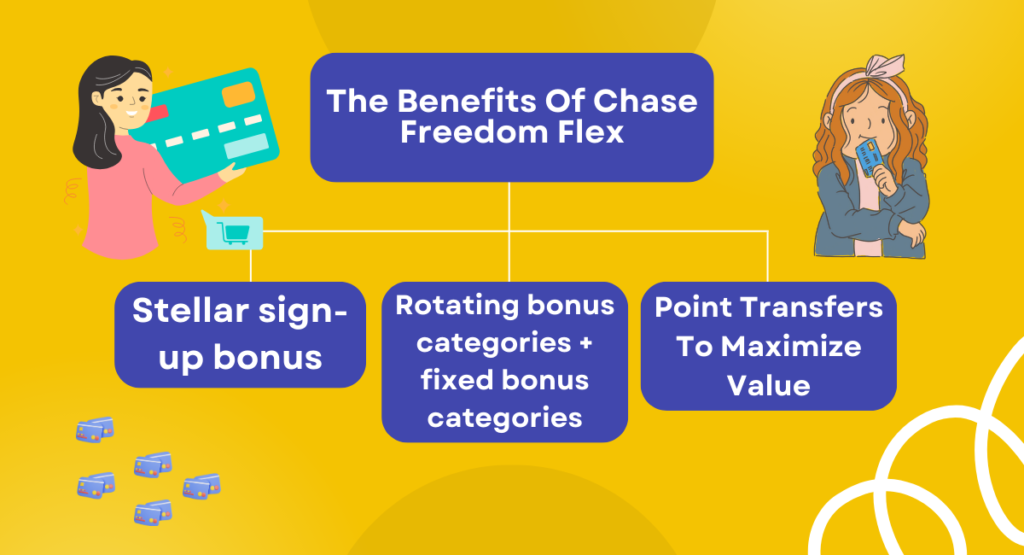

The Benefits Of Chase Freedom Flex

1. Stellar sign-up bonus

Obtain a $200 incentive on purchases totalling $500 within three months following account creation. That is about the best a no-annual-fee credit card can get.

2. Rotating bonus categories + fixed bonus categories

The 5% cash back applies to general categories that are frequented by a large number of individuals. Gas stations, grocery stores, department stores, wholesale organizations, and Amazon.com are all potential categories.

Numerous creditors will have the opportunity to accumulate substantial bonus rewards with minimal adjustment to their spending patterns. (However, quarterly activation of incentive categories is required.)

However, in addition to the 5% categories that change annually, the Chase Freedom Flex card provides year-round rewards in well-liked categories. Do you devote much of your monthly income to delivery and dining out?

Each time you use your Chase Freedom Flex card, you will get 3% cash back and 3% at the pharmacy. In contrast to the 5% bonus categories, which have a quarterly spending limitation of $1,500, the 3% earnings on drugstores and dining are unlimited.

3. Point Transfers To Maximize Value

Although Chase Ultimate Rewards points are generally valued at one cent each, several Chase cards offer the opportunity to redeem them for an additional 25% to 50% in value. You can maximize your rewards by transferring points from the Chase Freedom Flex to one of the following cards:

- When travel is redeemed for purchases made via the Chase online portal, 1.25 cents are credited to each Chase Sapphire Preferred Card and Ink Business Preferred Credit Card point balance.

- One-half cent is the value of each point accumulated through the Chase Sapphire Reserve in exchange for travel reservations made via Chase.

Additionally, approximately twelve hotel and airline loyalty programs, including those of Hyatt, United, Southwest, JetBlue, and British Airways, accept points transfers at a 1:1 ratio. The potential value of transferred points may be enhanced, contingent upon their utilization.

Remember that these other Chase cards impose annual fees, unlike Chase Freedom Flex.

How To Select The Best Card For International Travel?

When deciding which travel card is optimal, keep the following in mind:

- Look for a credit card with no foreign transaction fees: Credit cards do not impose foreign transaction fees on purchases conducted beyond the borders of the United States.

- Annual fees: Annual fees can be charged to credit cards with no foreign transaction fees; this should be considered when selecting a credit card.

- Rewards: Consider the various benefits and rewards accessible to cardholders who do not incur foreign transaction fees. For instance, using a travel rewards card to make travel-related purchases can help you accumulate points.

- Confirm your card will be accepted: Verify that your card is accepted at your travel destination before concluding that the card without foreign transaction fees is the most suitable option.

- Travel benefits: Consider applying for a credit card that offers travel benefits. Instances of such insurance policies include travel cancellation and baggage delay insurance.

In conclusion, although the Chase Freedom Flex is a commendable credit card for accumulating cash back on routine purchases, its 3% foreign transaction fee diminishes its suitability for international travel or overseas purchases.

Before applying, prospective cardholders should consider the advantages of cash back, introductory offers, and the absence of an annual fee to determine whether this card is consistent with their spending patterns and financial objectives. It may be more suitable for frequent international travellers to consider alternative Chase cards or competitors that do not charge foreign transaction fees.

Thank you for reading……

Read More: How Do You Transfer Chase Points To Another Person?